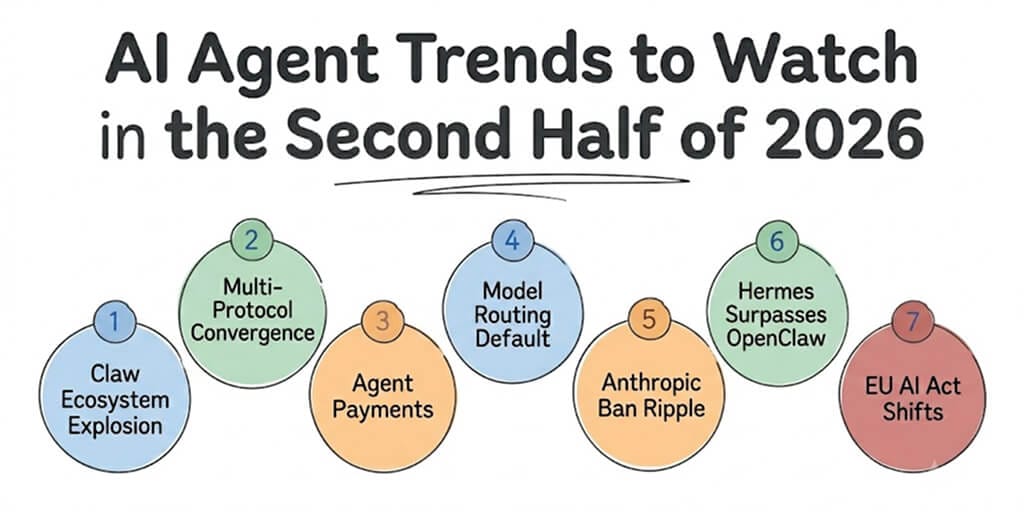

Seven specific shifts happening right now in the agent-building space. Not predictions. Evidence. And what each one means if you're building or buying.

I keep a document called "things that changed this month" for the AI agent space. In January 2026, it had 8 entries. In February, 14. By May, I stopped counting at 40.

The first half of 2026 has been the most chaotic, productive, and genuinely surprising period in the AI agent space since the concept went mainstream. Six new agent frameworks launched. Anthropic banned third-party tools from using Claude subscriptions. OpenClaw spawned an entire ecosystem of alternatives. MCP hit 78% enterprise adoption. An agent processed $73 million in on-chain transactions. The EU delayed its AI Act deadline... then partially un-delayed it.

If you're building, buying, or investing in AI agents, here are the seven AI agent trends that will define the second half of 2026. Not forecasts. Things already happening that are about to get bigger.

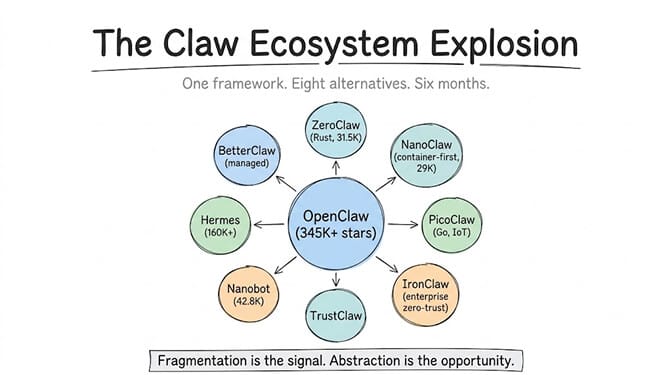

Trend 1: The "Claw" ecosystem is fragmenting faster than anyone expected

OpenClaw has 345,000+ GitHub stars. It's the most popular open-source agent framework in history. And it's fragmenting.

In the last six months, the ecosystem has spawned ZeroClaw (rewritten in Rust, 31,500 stars), NanoClaw (container-first, 29,000 stars), PicoClaw (Go, targeting IoT), IronClaw (enterprise zero-trust), TrustClaw, Nanobot (42,800 stars), and Hermes (160,000+ stars with a fundamentally different architecture).

What this means for H2 2026: The self-hosted agent category is splitting into niches. There will not be one framework to rule them all. The winners in this fragmentation are platforms that abstract the framework choice away entirely. You pick the capabilities you need. The platform handles which framework, which model, which hosting.

This is exactly what happened with web frameworks in 2015 to 2018. Rails, Django, Express, Flask, Spring... the ecosystem fragmented, and the winners were PaaS platforms that made the framework choice less important. Same pattern. Different technology.

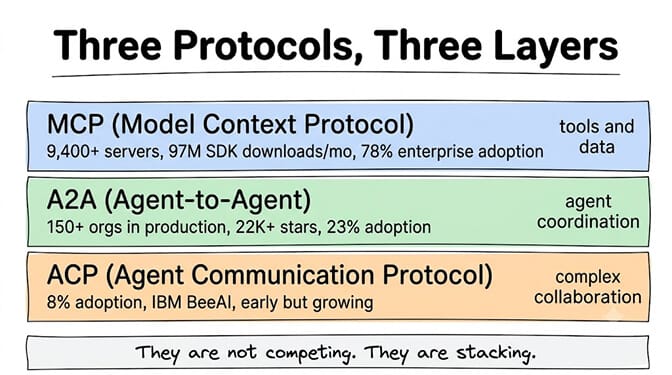

Trend 2: MCP, A2A, and ACP are settling into layers, not competitors

Six months ago, the protocol debate was: which one wins? Now the answer is clear: they're layers, not competitors.

MCP handles how agents connect to tools and data. 9,400+ servers. 97 million SDK downloads per month. 78% of enterprise teams use it. This is the settled standard for "agent talks to tool."

A2A handles how agents talk to other agents. 150+ organizations running it in production. 22,000+ GitHub stars. 23% enterprise adoption. Growing fast because multi-agent systems need a coordination protocol.

ACP is the early-stage layer for complex multi-agent collaboration. 8% adoption. IBM's BeeAI platform leads the push. Still finding its shape.

What this means for H2 2026: If you're building an AI agent platform, MCP support is table stakes. A2A support is a competitive advantage. ACP is worth watching but not worth building for yet. The teams that treat these as layers (not either/or choices) will build more capable agent systems. We broke down where each one fits in our A2A vs MCP vs ACP guide.

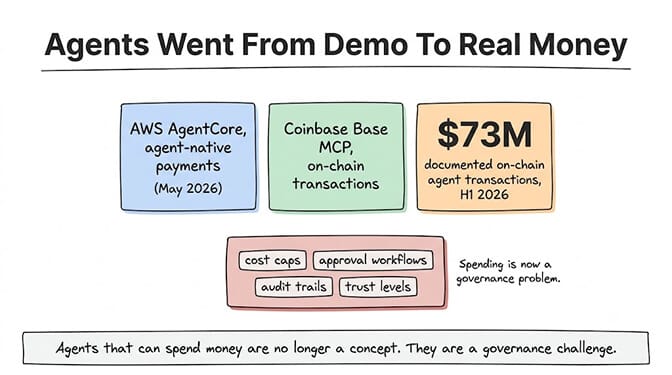

Trend 3: Agent payments went from demo to real money

AWS AgentCore launched agent-native payments in May 2026. Coinbase shipped Base MCP for on-chain agent transactions. Public data shows $73 million in documented on-chain agent transactions in H1 2026.

Agents that can spend money are no longer a concept. They're a governance challenge.

What this means for H2 2026: Every agent platform needs spending controls. Per-agent cost caps. Transaction approval workflows. Audit trails for every dollar spent. The platforms that treat agent spending as a first-class feature (not an afterthought) will win enterprise deals. The platforms that don't will lose them the first time an agent spends $5,000 on the wrong vendor.

BetterClaw already ships with per-agent cost caps and trust levels (Intern, Specialist, Lead) with action approval workflows. We built these before agent payments were real because we knew this was coming. The governance challenge is now.

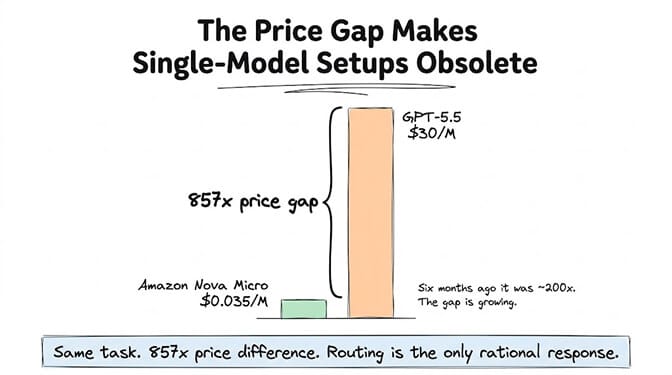

Trend 4: Model routing is the new default, not an optimization

The price gap between the cheapest and most expensive AI models is now 857x on output tokens (Nova Micro at $0.035 vs. GPT-5.5 at $30). Six months ago it was around 200x. The gap is growing, not shrinking.

Single-model setups are economically irrational at this spread. Using GPT-5.5 for a status check that Nova Micro handles identically is like chartering a private jet to cross the street.

Belitsoft's 2026 report found that the average enterprise runs 12 AI agents, expected to reach 20 by 2027. Salesforce's Connectivity Benchmark shows 89% of enterprises running agents across most or all teams. At that scale, model routing isn't an optimization. It's survival.

What this means for H2 2026: Platforms that don't support multi-provider BYOK with per-task model assignment will lose to platforms that do. Model routing cuts costs by 70 to 90%. Every CTO will be asking "why are we paying $600/month when we could pay $60?" by Q3. Here's how model routing reduces AI costs in practice.

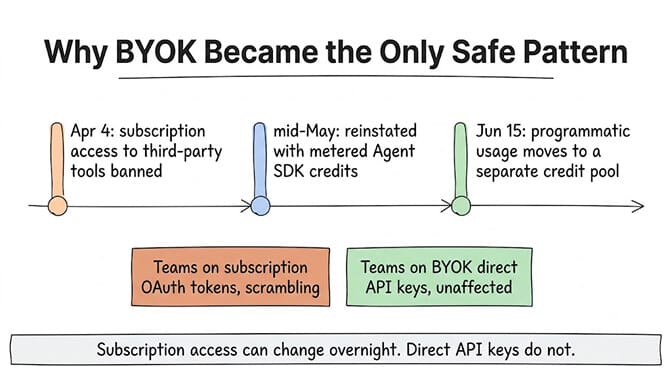

Trend 5: The Anthropic ban ripple effect is reshaping how developers pay for AI

On April 4, 2026, Anthropic banned Claude Pro/Max subscriptions from being used in third-party tools, including OpenClaw, Hermes, and most agent frameworks. The reasoning was straightforward: subscription plans were priced for human conversations, not always-on agents processing thousands of requests.

Then on June 1, 2026, Anthropic announced a further restructuring: splitting automated and interactive usage into separate pools. Credits for programmatic access must be manually claimed. No rollover.

Meanwhile, OpenAI moved in the opposite direction. Sam Altman explicitly stated OpenClaw is "flat available under ChatGPT paid plans." OpenAI offered two months of free Codex for enterprise users migrating from Claude.

What this means for H2 2026: BYOK and direct API keys are becoming the only reliable access pattern for agent builders. Subscription-based access can be revoked, restructured, or repriced without warning. Teams that built on subscription OAuth tokens are scrambling. Teams on BYOK with direct API keys were unaffected.

BetterClaw has been BYOK-only since launch. You paste your API key. You pay the provider directly. No middleman markup. No subscription dependency. When Anthropic changed terms, our users changed nothing.

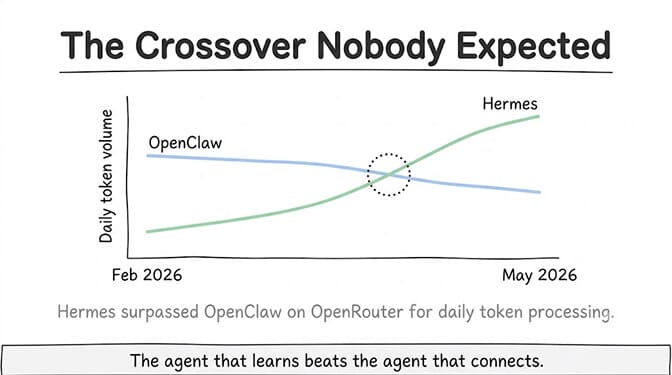

Trend 6: Hermes surpassed OpenClaw on daily token processing

Hermes Agent crossed 160,000+ GitHub stars. It launched February 25, 2026, and in under four months surpassed OpenClaw on OpenRouter for daily token processing volume.

The reason isn't more integrations (OpenClaw has far more). It's the architecture. Hermes has a closed-loop learning system that auto-creates reusable skills from completed tasks. The agent gets better the more you use it. OpenClaw's agent stays the same unless you manually update its configuration.

What this means for H2 2026: Persistent memory and self-improvement are becoming the differentiating features. The number of integrations matters less than whether the agent learns from past interactions. Expect every major framework to ship some form of skill auto-generation by Q4. For a detailed comparison of the two frameworks, our Hermes comparison covers architecture, pricing, and setup differences.

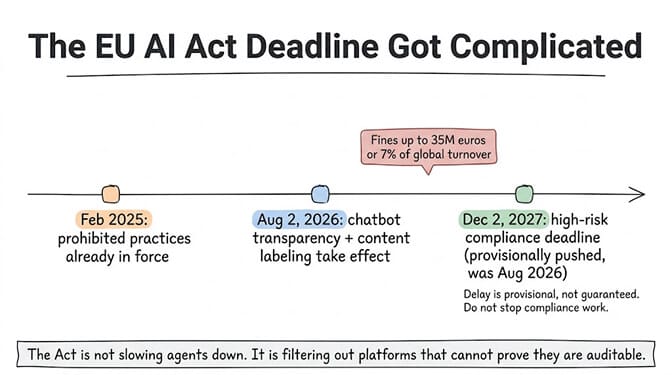

Trend 7: The EU AI Act deadline just got complicated

The original plan: August 2, 2026, all high-risk AI systems must demonstrate compliance with the EU AI Act. Fines up to 35 million euros or 7% of global turnover.

Then on May 7, 2026, EU lawmakers reached a provisional agreement to push the high-risk compliance deadline to December 2, 2027... a 16-month delay. But the formal adoption needs to happen before August 2, 2026, to take legal effect.

What's still happening in August 2026: Transparency obligations for chatbots take effect. AI-generated content labeling requirements apply (with a 4-month grace period to December 2026). Prohibited AI practices are already in force since February 2025.

What this means for H2 2026: Don't stop compliance work. The delay is provisional, not guaranteed. And even if high-risk deadlines shift, transparency and audit trail requirements are active now. Agent platforms that can demonstrate logging, monitoring, and audit trails will win enterprise procurement. Platforms that can't will be disqualified before the demo.

Gartner predicts 40% of enterprise apps will embed AI agents by end of 2026. IDC's FutureScape says 80% of developers will work with autonomous agents by 2030. The market is going there. Compliance determines who gets to participate.

The EU AI Act isn't slowing agents down. It's filtering out the platforms that can't prove their agents are auditable.

What all seven trends point to

The pattern across all seven trends is convergence toward managed, multi-provider, auditable platforms.

Framework fragmentation (trend 1) means abstraction wins. Protocol layering (trend 2) means integration depth wins. Agent payments (trend 3) mean governance wins. Model routing (trend 4) means multi-provider flexibility wins. The Anthropic ban (trend 5) means BYOK wins. Hermes growth (trend 6) means persistent memory wins. EU AI Act (trend 7) means audit trails win.

If you're building in this space, give BetterClaw a look. Multi-provider BYOK across 28+ providers with zero markup (trends 4 and 5). 200+ verified skills with 4-layer security audit (trend 7). Smart context management and per-agent cost caps (trends 3 and 4). Persistent memory with hybrid vector + keyword search (trend 6). Trust levels with action approval and kill switch (trend 3). Free plan with 1 agent and 500 credits a month. $49/month for Pro. 50+ companies in production including Carelon, Grainger, and Robert Half.

We publish this trends piece quarterly. The next update will be in September 2026. Bookmark this page and we'll update it.

Frequently Asked Questions

What are the biggest AI agent trends in 2026?

Seven major shifts are defining 2026: the open-source agent ecosystem fragmenting (OpenClaw spawning 8+ alternatives), MCP reaching 78% enterprise adoption as the standard agent-to-tool protocol, agent payments going live (AWS AgentCore, Coinbase Base MCP, $73M+ in on-chain transactions), model routing becoming default due to the 857x price gap between models, Anthropic's subscription ban pushing developers to BYOK, Hermes surpassing OpenClaw on daily token volume, and EU AI Act compliance reshaping enterprise procurement.

How big is the AI agent market in 2026?

Gartner predicts 40% of enterprise apps will embed AI agents by end of 2026. McKinsey estimates the addressable value of AI automation at $2.6 to $4.4 trillion. Salesforce's 2026 Connectivity Benchmark found 89% of enterprises are running AI agents across most or all teams. The average enterprise runs 12 AI agents, expected to reach 20 by 2027. Futurum Group data shows AI agents as a top technology priority increased 31.5% year-over-year.

How does the EU AI Act affect AI agent platforms?

The EU AI Act requires transparency, logging, and audit trails for AI systems operating in EU jurisdiction. The original high-risk compliance deadline was August 2, 2026, but EU lawmakers provisionally agreed to push it to December 2027. However, transparency obligations for chatbots and AI content labeling still take effect in August 2026. Fines can reach 35 million euros or 7% of global turnover. Agent platforms need audit trails, human oversight controls, and documented governance to qualify for enterprise procurement.

Is it still worth building on OpenClaw in 2026?

OpenClaw remains the most popular open-source agent framework (345K+ stars), but the ecosystem is fragmenting. Hermes surpassed OpenClaw on daily token volume. Nine CVEs were disclosed in four days in March 2026. Anthropic banned subscription access for OpenClaw agents. The framework is still powerful for developers who want full control, but the maintenance burden, security risks, and framework fragmentation are pushing many teams toward managed platforms like BetterClaw.

What should I prioritize when choosing an AI agent platform in H2 2026?

Five things, based on current market direction: multi-provider BYOK support (the Anthropic ban showed that single-provider dependency is risky), model routing capability (the 857x price gap makes single-model setups wasteful), audit trails and logging (EU compliance is coming regardless of deadline shifts), persistent memory (the Hermes crossover showed that agents that learn outcompete agents that don't), and spending controls (per-agent cost caps and approval workflows are essential as agents gain payment capabilities).